Financial Thanksgiving 2014 BlogMark TalercioNovember 24, 2014Ann Marsh, CFPB, finaid-org, Financial Planning Coalition, Financial Thanksgiving, FPA, LifeHappens, Mark Kantrowitz, NAPFA, NBER

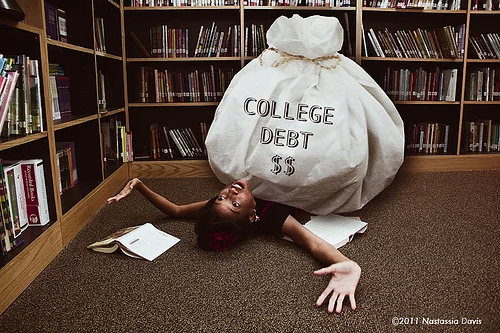

Student loans: What you need to know BlogMark TalercioSeptember 5, 2013College loans, education debt, finaid-org, Perkins loans, PLUS loans, refinance student debt, Sallie Mae, Stafford Loans, Student loans